Japanese Stocks Tumble, Leading Equities Selloff: Markets Wrap

2024-08-05

Global Markets Reel as Recession Fears Intensify

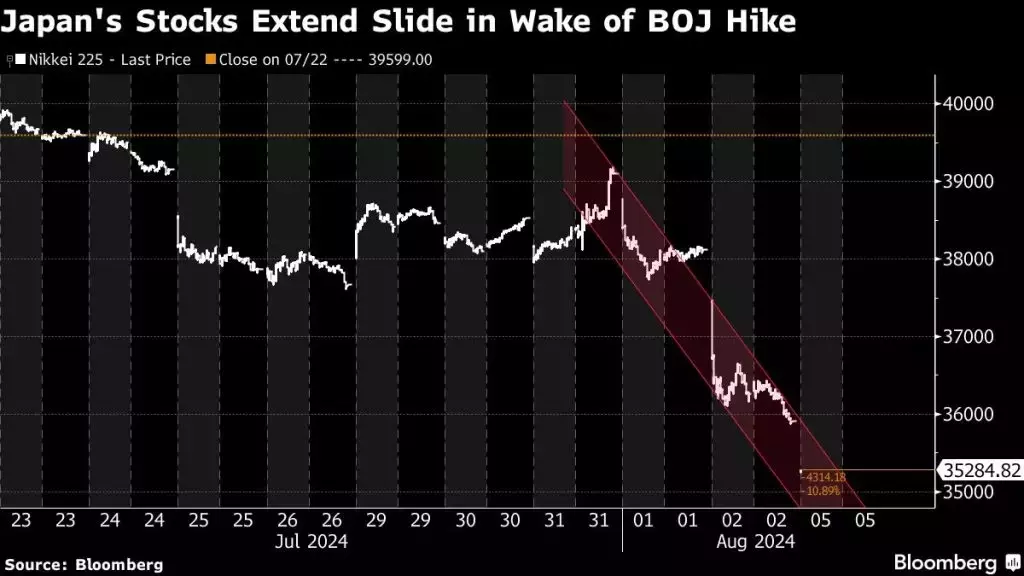

The global stock market selloff deepened on Monday, as concerns grew that the Federal Reserve is lagging behind in providing policy support for a slowing US economy, prompting investors to seek the safety of bonds. Japanese shares plunged for a third consecutive day, with traders pricing in more domestic rate hikes.

Navigating the Turbulent Tides of Global Markets

Shifting Sentiment and Recession Indicators

The price action in the markets underscores the rapid shift in sentiment away from expectations that the Federal Reserve will be able to engineer a soft landing for the US economy. Data released on Friday showed that US nonfarm payrolls recorded one of the weakest prints since the pandemic, and the jobless rate unexpectedly climbed above the Fed's year-end forecast, triggering a closely watched recession indicator. This has led to a growing consensus among investors that the Fed may be behind the curve in its policy support, potentially risking a deeper economic slowdown.Analysts have noted that the "conspiracy of 'risk off' triggers" is at play, with the Bank of Japan signaling more tightening and the Fed potentially being too slow to respond. The unwind of carry trades and recession fears have combined to significantly dampen risk appetite in the markets.

Plunging Japanese Stocks and Bond Yields

The moves in Japanese benchmark indexes have driven their drops to more than 20% - a loss that signals a bear market. The three-day losses are the worst since the 2011 tsunami and Fukushima nuclear meltdown. The sell-off in Japanese equities has been accompanied by a rally in Japanese government bonds, with the benchmark 10-year bond yield falling to its lowest level since April, slipping as much as 17 basis points to 0.785% on Monday.The bond market rally has not been limited to Japan, with New Zealand yields declining a similar amount and Australian bonds also seeing a significant drop, despite the Reserve Bank of Australia's policy meeting scheduled for the following day.

Commodities and Geopolitical Tensions

In the commodities market, oil prices extended their losses on Monday amid reports that Iran may strike Israel to avenge the assassinations of Hezbollah and Hamas officials. This worsening conflict in the Middle East risks adding more tumult to the already volatile markets, as investors brace for a turbulent second half of the year.The sell-off in global equities has been accompanied by a rise in market volatility, with the VIX Index - Wall Street's fear gauge - jumping to the highest level in almost 18 months. This heightened uncertainty is likely to persist as investors grapple with the prospect of a deeper economic slowdown and the potential for further geopolitical tensions.

Shifting Expectations and the Fed's Dilemma

Investors are increasingly concerned that the Federal Reserve's decision to hold interest rates at a two-decade high is jeopardizing the prospects of a soft landing for the US economy. Traders are now projecting the Fed will cut rates by more than a full percentage point in 2024, with an increased chance of an outsized 50-basis point cut in September.This shift in expectations has led some analysts to revise their forecasts, with UBS Group AG's wealth management unit changing its base case to rate cuts of 50 basis points in September and 25 basis points each in November and December, up from its previous projection of just half that amount by the end of the year.However, bond traders have a history of misjudging the direction of interest rates, at times overshooting in both directions and being caught off guard when the economy defies recession calls or inflation expectations. As such, the path forward for the Fed and the markets remains highly uncertain, with the potential for further volatility and surprises.

Monitoring the Chinese Economy

Investors will also be closely watching developments in the Chinese economy, as the government has laid out its priorities to spur consumer spending amid weak domestic demand. The release of the Caixin China services and composite activity data later on Monday will provide important insights into the health of the world's second-largest economy, following the unexpected contraction in manufacturing PMI last week.The coming week will be a busy one for economic data and central bank decisions, with the Bank of Australia, the Reserve Bank of India, and several Latin American central banks all set to announce their policy decisions. Investors will be closely monitoring these events for clues on the global economic outlook and the path forward for monetary policy.